Saturday, January 07, 2012

American Home Mortgage Servicing Inc. (AHMSI) Improper Move on Van Horne Home Gets $50,000 Rebuke from Judge

A bankruptcy judge has ordered one of the nation’s largest mortgage servicers to pay $50,000 to a Van Horne couple for seeking permission to foreclose on their house after failing to tell them their payments had increased.

American Home Mortgage Servicing Inc. (AHMSI) of Texas, which has gotten in trouble with regulators in several states, was ordered to pay $40,000 in punitive and $10,000 in compensatory damages to Alan and Kristine Wright by U.S. Bankruptcy Judge Paul Kilburg on Dec. 28.

The couple had filed for Chapter 13 bankruptcy protection in September 2008 with the intention of catching up on their monthly mortgage payments on their Van Horne home. Chapter 13 bankruptcy is often sought as a way to resolve a mortgage delinquency, according to Janet Hong, the Cedar Rapids attorney who represented the couple.

The bankruptcy plan protected the couple from losing their home as long as they kept up with the court-approved payment plan, but in on May 13, 2010, AHMSI filed a motion to lift the bankruptcy’s protective stay, saying that they were in default.

The motion was withdrawn by AHMSI, but the mortgage servicer filed a second motion about one year later again claiming that the Wrights were in default.

Without notice, AHMSI began placing mortgage payments from the couple in a “suspense account,” drawing from the account to make up the deficiency in each monthly until it was fully expended and returning the next payment, according to the judge’s ruling. The couple didn’t know their account was in arrears until they received the returned check. Their requests for a payment coupon book from AHMSI had been rejected more than once.

The couple eventually found through the court that their payments had been increased due to higher requirements for escrow — the money set aside by the mortgage servicer to pay things like property taxes and insurance — but they had not been notified.

Rest here…

Motion to Show Cause

American Home Mortgage Servicing Inc. (AHMSI) of Texas, which has gotten in trouble with regulators in several states, was ordered to pay $40,000 in punitive and $10,000 in compensatory damages to Alan and Kristine Wright by U.S. Bankruptcy Judge Paul Kilburg on Dec. 28.

The couple had filed for Chapter 13 bankruptcy protection in September 2008 with the intention of catching up on their monthly mortgage payments on their Van Horne home. Chapter 13 bankruptcy is often sought as a way to resolve a mortgage delinquency, according to Janet Hong, the Cedar Rapids attorney who represented the couple.

The bankruptcy plan protected the couple from losing their home as long as they kept up with the court-approved payment plan, but in on May 13, 2010, AHMSI filed a motion to lift the bankruptcy’s protective stay, saying that they were in default.

The motion was withdrawn by AHMSI, but the mortgage servicer filed a second motion about one year later again claiming that the Wrights were in default.

Without notice, AHMSI began placing mortgage payments from the couple in a “suspense account,” drawing from the account to make up the deficiency in each monthly until it was fully expended and returning the next payment, according to the judge’s ruling. The couple didn’t know their account was in arrears until they received the returned check. Their requests for a payment coupon book from AHMSI had been rejected more than once.

The couple eventually found through the court that their payments had been increased due to higher requirements for escrow — the money set aside by the mortgage servicer to pay things like property taxes and insurance — but they had not been notified.

Rest here…

Motion to Show Cause

IG Report on Bondi Firings of June Clarkson and Theresa Edwards – No Evidence of Wrongdoing

TALLAHASSEE — A long awaited report on the firings of two foreclosure fraud attorneys from Attorney General Pam Bondi’s office concluded that no one within the office acted improperly in dismissing Theresa Edwards and June Clarkson last spring.

“A review of the facts did not indicate that their forced resignation/termination was conducted in violation of any rule, policy or law,” the report states.

Edwards and Clarkson were making national headlines for exposing mortgage lenders and law firms for unsavory practices related to the foreclosure mess plaguing the state and country. But then Bondi’s office abruptly fired them at the end of May, leading to a public fight between the two lawyers and Bondi’s office.

The lawyers said the firings were political. Bondi’s office defended the action though, saying that the two attorneys kept inadequate case files and had essentially publicly vilified a company, Lender Processing Services, in a power point presentation to other lawyers about deceptive foreclosure practices.

Bondi’s office released a statement with the report, which was completed by Chief Financial Officer Jeff Atwater’s office, saying that the report confirmed that the firings were not political.

Rest here…

“A review of the facts did not indicate that their forced resignation/termination was conducted in violation of any rule, policy or law,” the report states.

Edwards and Clarkson were making national headlines for exposing mortgage lenders and law firms for unsavory practices related to the foreclosure mess plaguing the state and country. But then Bondi’s office abruptly fired them at the end of May, leading to a public fight between the two lawyers and Bondi’s office.

The lawyers said the firings were political. Bondi’s office defended the action though, saying that the two attorneys kept inadequate case files and had essentially publicly vilified a company, Lender Processing Services, in a power point presentation to other lawyers about deceptive foreclosure practices.

Bondi’s office released a statement with the report, which was completed by Chief Financial Officer Jeff Atwater’s office, saying that the report confirmed that the firings were not political.

Rest here…

Hedge fund with $100 million in Kentucky retirement funds fails

FRANKFORT — A hedge fund in which Kentucky Retirement Systems invested $100 million has failed and will be closing.

Arrowhawk Capital Partners of Darien, Conn., could not raise enough money from investors to succeed, said T.J. Carlson, KRS chief investment officer. KRS oversees $13 billion in retirement funds for state and local government employees.

KRS expects to get its $100 million back as Arrowhawk carefully unwinds its portfolio, Carlson said Thursday.

"That could change in the next few months, but as of right now, we do hope to get back the money we put in," he said.

Arrowhawk did not return a call seeking comment.

Read more here: http://www.kentucky.com/2012/01/05/2017395/hedge-fund-with-100-million-in.html#storylink=cpy

And who is Arrowhawk Capital Partner? Well, Morgan Stanley is involved.

Friday, January 06, 2012

CFPB mortgage complaint system is up and running

The CFPB is accepting mortgage complaints from consumers who have experienced difficulties in the housing market, including problems related to mortgage documents, mortgage servicers, and foreclosure.

As most people know, problems in the mortgage industry were a major cause of the 2008 financial crisis. As the nation’s consumer watchdog, the CFPB is here to make sure those in the mortgage industry are following Federal consumer financial laws.

To submit complaints, inquires, feedback, or just plain tell the CFPB about an experience they had with mortgages, consumers can:

- Call our toll-free phone number at 1-855-411-CFPB (2372)

- Visit us online

- Fax us at 1-855-237-2392

- Mail a letter to P.O. Box 4503, Iowa City, IA 52244

When we receive a consumer complaint, we review the complaint for completeness, jurisdiction, and duplication. We forward the complaint to the relevant financial institution for review and resolution. The institution has 15 days to provide a response to the CFPB. Institutions are expected to resolve and close all but the most complicated complaints within 60 days.

Throughout this process, consumers can log in to CFPB’s website to check the status of their complaints. If they are not satisfied with how their complaint was resolved, they can dispute the resolution.

General Electric subprime unit fraud-plagued; Ex-employees say GE ignored warnings from whistleblowers

For General Electric Co., hawking subprime mortgages was a long way from making light bulbs and jet engines.

That didn't stop the industrial giant from jumping into the subprime business in 2004, lending blue-chip respectability to the market for risky home loans by paying roughly half a billion dollars to buy California-based WMC Mortgage Corp.

What GE got in the bargain, former WMC employees say, was a place where erstwhile shoe salesmen, ex-strippers and even a former porn actress could sign on as sales reps and make big money pushing home loans. WMC's top salespeople earned a million dollars a year or more and lived fast, swigging $1,000 bottles of Cristal and wheeling around in $100,000 Ferraris and Bentleys.

In pursuit of these riches and perks, several ex-employees claim, many WMC sales staffers embraced fraud as a tool for pushing through loans that borrowers couldn’t afford.

Dave Riedel, a former compliance manager at WMC, says sales reps intent on putting up big numbers used falsified paperwork, bogus income documentation and other tricks to get loans approved and sold off to Wall Street investors.

One WMC official, Riedel claims, went so far as to declare: “Fraud pays.”

How well did GE address WMC’s fraud problems?

GE says it did plenty to deal with the issue. Some ex-employees counter that GE officials didn’t do enough to rein in illicit practices, despite warnings from Riedel and other whistleblowers inside the lender. GE dispatched emissaries to look into the problem, the ex-employees say, but their efforts were too little, too late.

“They sent in people we thought were going to bring us back in the right direction,” Victor Argueta, a former risk analyst at WMC, says. “But it just never happened.”

By 2007, WMC was bleeding bad loans and red ink. General Electric shut the lender and reported related losses totaling more than $1 billion.

US home mortgage bond investors left holding the bag: May want pension funds to pay part of the state AGs settlement instead of banks

Investors in US home mortgage bonds may have to swallow losses as part of a wide-ranging settlement being discussed between leading banks and the Obama administration to resolve allegations of foreclosure misdeeds, people familiar with the matter said.

Participants in the discussions cautioned that a final agreement remains weeks away and that the terms being discussed could change. However, they said it is likely banks would be able to reduce loan principal on mortgages owned by investors through mortgage-backed bonds.

Source: Financial Times

Biloxi Buzz for Friday

Walmart Dumped By Pension Fund Over Poor Worker Conditions

Obama to unveil summer-jobs initiative

Obama to unveil summer-jobs initiative

Three charged in John Doe investigation of Walker aides — By Daniel Bice of the Journal Sentinel — Three individuals - including a former top aide to Gov. Scott Walker - were charged Thursday with felonies as part of the ongoing John Doe investigation into Walker staffers.

Capital One Faces Suit Over Short Sales

SANTA ANA, Calif. (CN) - Homeowners say in a class action that Capital One illegally made them pay thousands of dollars in deficiency contributions after short sales of their homes, though the state prohibited that in 2010.

Then-Gov. Arnold Schwarzenegger signed Senate Bill 931 into law in late 2010 to reduce foreclosures and boost short sales.

Before the law took effect in January 2011, homeowners had no incentive to short sell their homes because while lenders could not obtain a deficiency judgment on foreclosed properties, they could go after homeowners who sold short.

"However, it quickly became apparent that where there was a second mortgage, the junior lien holder often refused to release the lien and the short sale never went through," according to the complaint.

"In February 2011, SB 458 was introduced, and on July 15, 2011, it was signed into law on an emergency basis. Section (a) of SB 458 expanded SB 931's prohibition on obtaining a deficiency judgment to junior lien holders. Additionally, Section (b) of SB 458 further mandate that a 'holder of a note shall not require the trustor, mortgagor, or maker of the note to pay any additional compensation, aside from the proceeds of the sale, in exchange for the written consent to the sale.' ...

"Capital One has refused to comply with SB 458. In clear violation of the statute's unambiguous prohibition, Capital One has illegally required California borrowers to pay the deficiency on their mortgages, in addition to 'the proceeds of the sale, in exchange for [Capital One's] written consent to the sale.' As a result, Capital One has generated substantial revenues from the collection of deficiencies from California-based borrowers in connection with completing short sales". (Brackets in complaint.)

Lead plaintiff Roni Teson says Capital One came after her for a $60,000 deficiency contribution on her Rancho Cucamonga home, and refused to approve a short sale offer of $570,000, even after her Realtor reminded the bank holding company of the new law.

Teson had been diagnosed with stage IV breast cancer, was on disability and could no longer keep up her mortgage payments, according to the complaint, whose other named plaintiff is Laurie Hatfield.

The complaint states: "A 'short sale' is when a borrower owes more than his/her house is worth and the bank allows the borrower to sell the house for less than is owed on the property. The incentive to do nothing but await a foreclosure - rather than undergo a short sale - was believed to be driving California's spiraling foreclosure rate, which in turn was only further reducing the equity of California's homeowners and preventing real property values from recovering."

Then-Gov. Arnold Schwarzenegger signed Senate Bill 931 into law in late 2010 to reduce foreclosures and boost short sales.

Before the law took effect in January 2011, homeowners had no incentive to short sell their homes because while lenders could not obtain a deficiency judgment on foreclosed properties, they could go after homeowners who sold short.

"However, it quickly became apparent that where there was a second mortgage, the junior lien holder often refused to release the lien and the short sale never went through," according to the complaint.

"In February 2011, SB 458 was introduced, and on July 15, 2011, it was signed into law on an emergency basis. Section (a) of SB 458 expanded SB 931's prohibition on obtaining a deficiency judgment to junior lien holders. Additionally, Section (b) of SB 458 further mandate that a 'holder of a note shall not require the trustor, mortgagor, or maker of the note to pay any additional compensation, aside from the proceeds of the sale, in exchange for the written consent to the sale.' ...

"Capital One has refused to comply with SB 458. In clear violation of the statute's unambiguous prohibition, Capital One has illegally required California borrowers to pay the deficiency on their mortgages, in addition to 'the proceeds of the sale, in exchange for [Capital One's] written consent to the sale.' As a result, Capital One has generated substantial revenues from the collection of deficiencies from California-based borrowers in connection with completing short sales". (Brackets in complaint.)

Lead plaintiff Roni Teson says Capital One came after her for a $60,000 deficiency contribution on her Rancho Cucamonga home, and refused to approve a short sale offer of $570,000, even after her Realtor reminded the bank holding company of the new law.

Teson had been diagnosed with stage IV breast cancer, was on disability and could no longer keep up her mortgage payments, according to the complaint, whose other named plaintiff is Laurie Hatfield.

The complaint states: "A 'short sale' is when a borrower owes more than his/her house is worth and the bank allows the borrower to sell the house for less than is owed on the property. The incentive to do nothing but await a foreclosure - rather than undergo a short sale - was believed to be driving California's spiraling foreclosure rate, which in turn was only further reducing the equity of California's homeowners and preventing real property values from recovering."

Former Florida assistant AG’s role on ethics complaint committee raises questions

TAMPA — Erin Cullaro, a former assistant attorney general fired after moonlighting for a “foreclosure mill,” continues to serve on a committee that investigates ethics complaints.

Some lawyers and consumer advocates question whether Cullaro belongs on the Florida Bar Association committee.

“The bar’s self-monitoring leaves much to be desired,” said Lisa Epstein of Foreclosure Hamlet, which tracks foreclosure fraud.

Cullaro, who worked for the state attorney general’s office in Tampa, was fired in April after a reprimand by Gov. Rick Scott’s office over variations of her signature on documents.

The attorney general’s office had reprimanded Cullaro in 2010 for notarizing documents on behalf of a foreclosure mill the office was investigating.

Check out the rest from TBO here…

Some lawyers and consumer advocates question whether Cullaro belongs on the Florida Bar Association committee.

“The bar’s self-monitoring leaves much to be desired,” said Lisa Epstein of Foreclosure Hamlet, which tracks foreclosure fraud.

Cullaro, who worked for the state attorney general’s office in Tampa, was fired in April after a reprimand by Gov. Rick Scott’s office over variations of her signature on documents.

The attorney general’s office had reprimanded Cullaro in 2010 for notarizing documents on behalf of a foreclosure mill the office was investigating.

Check out the rest from TBO here…

Thursday, January 05, 2012

DAVID J. STERN (enterprises) SUES DAVID J. STERN: David Stern Investors Admit Foreclosure Documents Were Forged

Mortgage Fraud

Law Offices of David J. Stern

ProVest

PTA

Action Date: January 4, 2012

Location: FT. Lauderdale, FL

In the lawsuit filed by DJSP Enterprises against David J. Stern and the Law Offices of David J. Stern, there are also allegations involving ProVest, the process server used by Stern and most of the other major foreclosure mills hired by Lender Processing Services in over 20 states.

The allegations regarding ProVest are found in paragraphs 36-38:

36. Prior to the Transaction, the Seller Defendants also knowingly and systematically inflated their process of service costs to the Court. Specifically, Seller Defendants engineered a fraudulent scheme whereby they directed their process servicing work to a process servicing company called ProVest. The Seller Defendants caused each file to generate four or five separate fees for service of process regardless of whether service of process on multiple defendants was necessary or appropriate and regardless of whether service of process for multiple defendants could be achieved at the same address.

37. In exchange for receiving these inflated service of process fees, ProVest, in turn, routinely referred back to PTA servicing requests for “skip tracing” to locate defendants for whom ProVest purportedly did not have accurate street address information to effect service of process. ProVest “hired” and paid fees to PTA for “skip tracing” services despite the fact that ProVest had the ability and resources to perform “skip tracing” itself and routinely did so itself.

38. The Seller Defendants’ arrangement with ProVest amounted to a kickback scheme. DS Law padded and inflated its process servicing costs which were billed to its clients and added to the court costs assessed to foreclosure defendants. In exchange for feeding this work to ProVest, PTA earned manufactured “skip tracing” fees which inflated PTA’s revenues and profits and which represented another way in which the Seller Defendants artificially inflated the revenues of the Target Business prior to the Transaction.

And there is more....

Stern pocketed some $60 million from that deal. The investors got the company and all its documents, internal procedures and everything you would need in order to find out what really happened within the Stern document mill.

A little after 8 AM EST today, a filing went up on the SEC’s Edgar database. It’s a Complaint in lawsuit, dated yesterday.

The lawsuit is by the investors suing Stern for lying to them about the activities of the document mill and misleading them into believing they were buying a legitimate business instead of a criminal enterprise. Unlike a regular plaintiff or an Attorney General who is dependent on obtaining documents and information FROM the target of their ire via discovery of subpoena or search warrant, these plaintiffs apparently have all the info they need already in hand, because they bought the company.

FDL

DjspComplaint

djsp8k

Wednesday, January 04, 2012

Biloxi Buzz for Wednesday

3 In-Laws of Afghan Girl, 15, Are Held in Her Torture — KABUL, Afghanistan — The Afghan girl's nails had been pulled out, her skin on her ear and nose had been twisted with pliers, and she had been kept in a dark, filthy basement bathroom without proper food or water for five months …

US Closes 2011 With Record $15.22 Trillion In Debt, Officially At 100.3% Debt/GDP, $14 Billion From Breaching Debt Ceiling — While not news to Zero Hedge readers who knew about the final debt settlement of US debt about 10 days ahead of schedule, it is now official: according to the US Treasury …

Fraudclosure | Largo Man Nearly Loses His Home Over 80 Cents

Shannon Behnken from WFLA in Tampa did a story yesterday about a homeowner in Largo, Florida who pressed the wrong number on his phone while making a electronic modification payment over the telephone. This little mistake caused Bank of America to kick him out of the modification program he was in and begin foreclosure proceedings even after he mailed them the check for the 80 cents

The Media And The Minnesota AG Stop Citi From Foreclosing On Nancy Gosselin

In a last-minute move, Citi- Mortgage called off the foreclosure sale of a St. Louis Park house whose owner battled to stay in her home with the support of the Minnesota attorney general.

Nancy Gosselin was scheduled to lose her house in a sheriff’s auction scheduled for Tuesday, even though an investigation by the attorney general determined that at most, she had missed one payment of $584 more than two years ago.

After Gosselin was featured in a Whistleblower column on Nov. 13, CitiMortgage postponed the foreclosure for a month. Then, this week, Gosselin got the good news.

“It was canceled,” Mark Rodgers, director of Citi public affairs, said in an e-mail to the Star Tribune on Thursday. “This matter has been resolved.”

Read more here

You can also read the previous story here

Nancy Gosselin was scheduled to lose her house in a sheriff’s auction scheduled for Tuesday, even though an investigation by the attorney general determined that at most, she had missed one payment of $584 more than two years ago.

After Gosselin was featured in a Whistleblower column on Nov. 13, CitiMortgage postponed the foreclosure for a month. Then, this week, Gosselin got the good news.

“It was canceled,” Mark Rodgers, director of Citi public affairs, said in an e-mail to the Star Tribune on Thursday. “This matter has been resolved.”

Read more here

You can also read the previous story here

Tuesday, January 03, 2012

Former Ameriquest Mortgage fired after he reported illegal activity, sued under the whistleblower provision of the Sarbanes-Oxley Act 2002

William McCloskey worked for Ameriquest from November 2004 till March 2005. William was fired after he reported illegal activity behind the walls of his Ameriquest branch, which virtually mirrored all of the widespread reports about the company (to local detectives, the PA Attorney General, the S.E.C. and the F.B.I).

William sued Ameriquest Mortgage Company under the whistleblower provision of the Sarbanes Oxley Act of 2002. The act pertained to publicly traded companies and issuers of securities under Section 15(d) and 12h-3 of the Securities and Exchange Act of 1934. Ameriquest was the largest issuer of asset-backed securities in the world during the refinance boom.William articulated how Ameriquest originated, processed and loosely underwrote toxic mortgages and then securitized them through their own subsidiary (Ameriquest Mortgage Securities) before the Department of Labor and the S.E.C. in McCloskey vrs Ameriquest Mortgage Company (2005-SOX-093).

Unfortunately, William ultimately lost the suit because of a technicality (he did not file his initial complaint with OSHA within 90-days). However, William thoroughly articulated how Ameriquest perpetrated the largest securities fraud scheme in the history of the United States. The securities fraud scheme was one of the biggest contributors to the collapse of the nation's markets and economy in September 2008. All of the bad paper issued by Ameriquest Mortgage Securities made its way around the world as collateralized debt obligations.

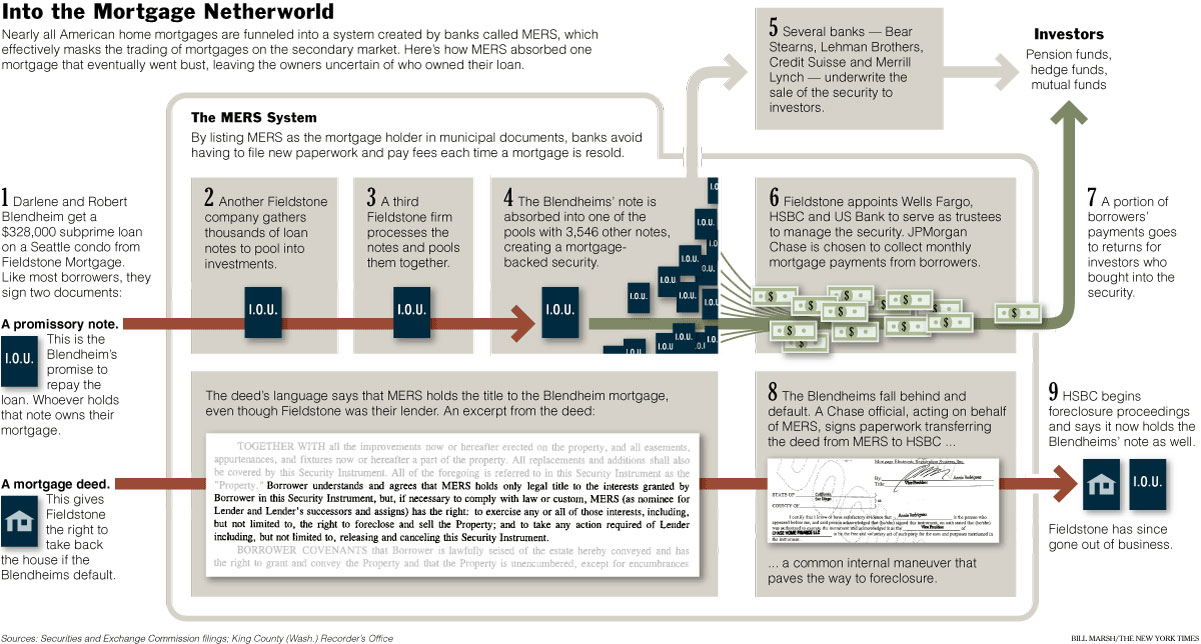

The shell game: Has portion of your mortgage payment been applied to your loan or to the securitization trust?

See above chart of the MERS system and how this particular portion of the homeowner's mortgage payment went to the returns to the investors who bought into the security.

Which begs the question: Have many of the portions of homeowners' mortgage payments actually going to the payoff the 15 or 30 term loan or going to the pay the investors in the securitization trust? Well, there is the force placed insurance probe where the banks charge more money for homeowners for insurance,

and now we learn of the Feds probing possible double dipping billing by banks. Why the Feds are probing the banks of double-dipping billing of escrow fees? From the questioning from the U.S. bankruptcy trustee from the DOJ. Check out this article that I posted in May of the U.S. bankruptcy trustee findings:NY Times:

The other problematic area showing up in the trustees’ inquiries relates to what Mr. White calls improper default servicing fees. These include charges for legal work, property inspections, insurance and appraisals.

Often, the fees charged to troubled borrowers are not even specified. Trustee program officials found a defaulted borrower who was charged $10,260.50 in “prior service fees” with zero documentation. In another case, a borrower fell behind after the lender doubled his escrow payments with no explanation or justification. Then the bank filed a motion to lift the bankruptcy stay so that it could foreclose.

“In fewer than 20 judicial districts,” Mr. White said, “we have identified hundreds of facial deficiencies, including cases in which we seek to investigate inflated or improper escrow charges and cases in which the mortgage servicer sought relief from stay so it could foreclose on a debtor’s home.”

Mistakes happen, of course. And loan servicers like to contend that if errors occur, they are rare and honestly made. But after sifting through the data produced by this investigation, Mr. White disagreed that problems are rare. “In Senate testimony, an executive from Countrywide said its error rate was 1 percent,” Mr. White recalled. “The mortgage servicer industry error rate might be 10 times higher, based on the number of cases we are looking at.”

Citigroup Inc. Hit By Iran's Central Bank Lawsuit

Iran’s central bank Bank Markazi is going to file a lawsuit in US Federal Court against Citigroup Inc. (NYSE:C) to release the frozen assets deposited by Clearstream Banking SA in Citibank.

The bank froze $2 billion assets in 2008 as the victims of international terrorism sought the fund as partial payments.

Bank Markazi said that it is illegal on the part of Citigroup Inc. (NYSE:C) to freeze the assets, as the move violates US law.

The bank froze $2 billion assets in 2008 as the victims of international terrorism sought the fund as partial payments.

Bank Markazi said that it is illegal on the part of Citigroup Inc. (NYSE:C) to freeze the assets, as the move violates US law.

Monday, January 02, 2012

Let's play "Find The Fraud"

Renown fraud examiner, Marie McDonnell, noted in her Phillips-Tehiva forensics report on page 13 (TEHIVA FORECLOSURE FORENSICS & EXHIBITS (MTM), 12.26.2011) that:

“(23) Moreover, the individual who executed the Assignment, Kathy Smith (“Smith”), is not an employee of Sand Canyon Corporation. Sand Canyon is located in Irvine, California whereas the Assignment was executed and notarized in Jacksonville, Florida.

(24) On information and belief, Smith works for Lender Processing Services (“LPS”) which is headquartered in Jacksonville, Florida. Linda Bayless, the Notary Public who witnessed

Smith’s signature, indicates in her jurat that this document was executed before her in

Jacksonville, Florida.

Smith’s signature, indicates in her jurat that this document was executed before her in

Jacksonville, Florida.

(25) The Assignment of Mortgage referenced herein executed by Kathy Smith is the questioned “breeder document” from which all other documents necessary to complete the foreclosure, sale, and transfer of the Tehiva Property to Wells Fargo Bank, NA a National Association as Trustee for Soundview Home Loan Trust 2007-OPT2, Asset-Backed Certificates, Series 2007-OPT2 arise.

Feds Probe $150 Million Double Billing Scheme By Banks

Federal investigators are looking into allegations that banks have wrongly pocketed tens of millions of dollars from troubled homeowners by double-billing for mortgage escrow fees, The Post has learned.

Exactly how much in phony profits the banks may have pocketed from this alleged practice is not known, but an analysis by The Post of bankruptcy cases in 2011 shows it could range higher than $150 million for just the new cases filed this year.

The problem has gotten so out of hand that lawyers and accountants at the New York City office of US Trustee — charged with protecting the integrity of US bankruptcy courts — are poring over local Chapter 13 bankruptcy cases for evidence of wrongdoing.

The federal investigators were tipped to the alleged practice by metro area bankruptcy lawyers. Cases specifically involved Wells Fargo and GMAC Mortgage, but lawyers say most banks had double-dipped.

“It seems prevalent, and it’s a moneymaking machine,” David Shaev, a Manhattan bankruptcy defense lawyer, said of the banks’ double-dipping.

Westchester bankruptcy defense lawyer Linda Tirelli says 75 percent of her clients face escrow double-billing by their lender or mortgage servicer, for amounts up to $2,800.

Here’s how the double-dipping scam can be pulled off.

Many homeowners opt to pay part of their property taxes and homeowners insurance with their mortgage every month. The funds are then put into an escrow account and used to periodically pay the taxes and insurance.

Read more here:

Exactly how much in phony profits the banks may have pocketed from this alleged practice is not known, but an analysis by The Post of bankruptcy cases in 2011 shows it could range higher than $150 million for just the new cases filed this year.

The problem has gotten so out of hand that lawyers and accountants at the New York City office of US Trustee — charged with protecting the integrity of US bankruptcy courts — are poring over local Chapter 13 bankruptcy cases for evidence of wrongdoing.

The federal investigators were tipped to the alleged practice by metro area bankruptcy lawyers. Cases specifically involved Wells Fargo and GMAC Mortgage, but lawyers say most banks had double-dipped.

“It seems prevalent, and it’s a moneymaking machine,” David Shaev, a Manhattan bankruptcy defense lawyer, said of the banks’ double-dipping.

Westchester bankruptcy defense lawyer Linda Tirelli says 75 percent of her clients face escrow double-billing by their lender or mortgage servicer, for amounts up to $2,800.

Here’s how the double-dipping scam can be pulled off.

Many homeowners opt to pay part of their property taxes and homeowners insurance with their mortgage every month. The funds are then put into an escrow account and used to periodically pay the taxes and insurance.

Read more here:

Bank fraud: Wells Fargo, American Home Mortgage Servicing, Inc

Fraud Digest:

Bank Fraud

American Home Mortgage Servicing

Sand Canyon Corporation

Kathy Smith

Soundview Home Loan Trust, 2007-OPT2

Wells Fargo Bank, N.A.

Action Date: January 1, 2012

Location: Maui, HI

On January 2, 2012, Wells Fargo Bank and American Home Mortgage Servicing, Inc. (“AHMSI”) will attempt to force the Tehiva/Phillips family from their family home on 5305 Hana Highway in Maui, Hawaii. This has been the family home for over 100 years.

Wells Fargo is acting as the Trustee for an RMBS Trust, Soundview Home Loan Trust 2007-OPT2. AHMSI is acting as the servicer for the trust.

Wells Fargo and AHMSI have relied on a fraudulent Mortgage Assignment in this foreclosure eviction.

The Assignment is dated June 24, 2010 and was signed by Kathy Smith in Duval County, Florida. Smith purports to be a corporate officer (Assistant Secretary) of Sand Canyon Corporation.

Kathy Smith is not and has never been employed by Sand Canyon Corporation; she is actually employed by AHMSI in its Jacksonville, FL (Duval County) office.

On Hillsborough County, FL, document 2010350478, Kathy Smith swore she was an employee of AHMSI on October 1, 2010.

On Hillsborough County, FL document 20100057228, Kathy Smith swore she was Assistant Secretary of AHMSI on February 8, 2010.

In the Memorandum Decision of the Bankruptcy Court for the District of Arizona in the matter of the bankruptcy of Anthony Tarantola, Case No. 4:09-bk-09703-EWH, Kathy Smith is referred to on Page 5, lines 8-9, as the Assistant Secretary of AHMSI.

To aid in foreclosures, Kathy Smith has used all of the following different job titles:

• Assistant Secretary and Vice President, Ameriquest Mortgage Company (February 3, 2010);

• Assistant Secretary and Vice President, Citi Residential, Inc., Attorney-in-Fact for Ameriquest Mortgage Company (April 12, 2010);

• Attorney-in-Fact, Argent Mortgage Corporation (January 13, 2010);

• Assistant Secretary, Citibank, N.A., as Trustee for American Home Mortgage Asset Trust 2006-3 Mortgage-Backed Pass-Through Certificates, Series 2006-3; (January 13, 2010);

• Assistant Secretary, Deutsche Bank National Trust Company as Indenture Trustee for American Home Mortgage Investment Trust 2006-3, Mortgage-Backed Notes, Series 2006-3 (January 13, 2010);

• Attorney-in-Fact, New Century Mortgage Corporation (January 19, 2010);

• Assistant Secretary, Sand Canyon Corporation f/k/a Option One Mortgage Corporation (April 12, 2010)

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for American Brokers Conduit (February 25, 2010);

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for American Home Mortgage (February 18, 2010);

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for American Home Mortgage Acceptance (January 25, 2010);

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for Beazer Mortgage Corporation (January 13, 2010);

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for HomeBanc Mortgage Corporation (January 11, 2010); and

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for Taylor, Bean & Whitaker Mortgage Corporation (May 7, 2010).

The President of Sand Canyon Corporation, Dale M. Sugimoto, submitted a sworn Declaration signed on March 18, 2009, stating that Sand Canyon Corporation did not own or service any residential real estate mortgages. Despite this sworn statement of the company president, the Assignment in the Tehiva/Phillips foreclosure has Kathy Smith, purporting to act as an officer of Sand Canyon, to transfer the Tehiva/Phillips mortgage to the Soundview Trust. The Sugimoto Declaration was submitted in bankruptcy court for the Eastern District of Louisiana, New Orleans Division, as document 52-3, in the case of Ron Wilson, Case No. 10-51328.

Kathy Smith is also not listed as an officer of Sand Canyon Corporation in the Florida corporate records, nor did Sand Canyon have offices in Florida, where the Assignment was notarized.

The closing date of the Soundview Trust 2007-OPT2 was July 10, 2007. The trust was not authorized to acquire mortgages after this date; and certainly was not authorized to ever acquire any non-performing mortgages.

For all of the reasons set forth above, Wells Fargo and AHMSI should immediately cease their attempts to seize the Tehiva/Phillips home. Wells Fargo should be required to produce Kathy Smith in court in Hawaii and to produce the records of the trust showing that the trust acquired the Tehiva/Phillips mortgage in 2010 as represented by Smith.

American Home Mortgage Servicing

Sand Canyon Corporation

Kathy Smith

Soundview Home Loan Trust, 2007-OPT2

Wells Fargo Bank, N.A.

Action Date: January 1, 2012

Location: Maui, HI

On January 2, 2012, Wells Fargo Bank and American Home Mortgage Servicing, Inc. (“AHMSI”) will attempt to force the Tehiva/Phillips family from their family home on 5305 Hana Highway in Maui, Hawaii. This has been the family home for over 100 years.

Wells Fargo is acting as the Trustee for an RMBS Trust, Soundview Home Loan Trust 2007-OPT2. AHMSI is acting as the servicer for the trust.

Wells Fargo and AHMSI have relied on a fraudulent Mortgage Assignment in this foreclosure eviction.

The Assignment is dated June 24, 2010 and was signed by Kathy Smith in Duval County, Florida. Smith purports to be a corporate officer (Assistant Secretary) of Sand Canyon Corporation.

Kathy Smith is not and has never been employed by Sand Canyon Corporation; she is actually employed by AHMSI in its Jacksonville, FL (Duval County) office.

On Hillsborough County, FL, document 2010350478, Kathy Smith swore she was an employee of AHMSI on October 1, 2010.

On Hillsborough County, FL document 20100057228, Kathy Smith swore she was Assistant Secretary of AHMSI on February 8, 2010.

In the Memorandum Decision of the Bankruptcy Court for the District of Arizona in the matter of the bankruptcy of Anthony Tarantola, Case No. 4:09-bk-09703-EWH, Kathy Smith is referred to on Page 5, lines 8-9, as the Assistant Secretary of AHMSI.

To aid in foreclosures, Kathy Smith has used all of the following different job titles:

• Assistant Secretary and Vice President, Ameriquest Mortgage Company (February 3, 2010);

• Assistant Secretary and Vice President, Citi Residential, Inc., Attorney-in-Fact for Ameriquest Mortgage Company (April 12, 2010);

• Attorney-in-Fact, Argent Mortgage Corporation (January 13, 2010);

• Assistant Secretary, Citibank, N.A., as Trustee for American Home Mortgage Asset Trust 2006-3 Mortgage-Backed Pass-Through Certificates, Series 2006-3; (January 13, 2010);

• Assistant Secretary, Deutsche Bank National Trust Company as Indenture Trustee for American Home Mortgage Investment Trust 2006-3, Mortgage-Backed Notes, Series 2006-3 (January 13, 2010);

• Attorney-in-Fact, New Century Mortgage Corporation (January 19, 2010);

• Assistant Secretary, Sand Canyon Corporation f/k/a Option One Mortgage Corporation (April 12, 2010)

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for American Brokers Conduit (February 25, 2010);

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for American Home Mortgage (February 18, 2010);

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for American Home Mortgage Acceptance (January 25, 2010);

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for Beazer Mortgage Corporation (January 13, 2010);

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for HomeBanc Mortgage Corporation (January 11, 2010); and

• Assistant Secretary, Mortgage Electronic Registration Systems, Inc., as Nominee for Taylor, Bean & Whitaker Mortgage Corporation (May 7, 2010).

The President of Sand Canyon Corporation, Dale M. Sugimoto, submitted a sworn Declaration signed on March 18, 2009, stating that Sand Canyon Corporation did not own or service any residential real estate mortgages. Despite this sworn statement of the company president, the Assignment in the Tehiva/Phillips foreclosure has Kathy Smith, purporting to act as an officer of Sand Canyon, to transfer the Tehiva/Phillips mortgage to the Soundview Trust. The Sugimoto Declaration was submitted in bankruptcy court for the Eastern District of Louisiana, New Orleans Division, as document 52-3, in the case of Ron Wilson, Case No. 10-51328.

Kathy Smith is also not listed as an officer of Sand Canyon Corporation in the Florida corporate records, nor did Sand Canyon have offices in Florida, where the Assignment was notarized.

The closing date of the Soundview Trust 2007-OPT2 was July 10, 2007. The trust was not authorized to acquire mortgages after this date; and certainly was not authorized to ever acquire any non-performing mortgages.

For all of the reasons set forth above, Wells Fargo and AHMSI should immediately cease their attempts to seize the Tehiva/Phillips home. Wells Fargo should be required to produce Kathy Smith in court in Hawaii and to produce the records of the trust showing that the trust acquired the Tehiva/Phillips mortgage in 2010 as represented by Smith.

Sunday, January 01, 2012

BofA throws “Preservation Specialist” under the bus, contractor arraigned for burglary of home

A Martinsburg man contracted by Bank of America to cut grass at a home a day after its foreclosure was arraigned on one count of daytime burglary Wednesday after he allegedly entered the house and rifled through the family’s personal belongings.

Warren Edward Brown, 30, of Herman Lane, was later released after posting $15,000 bail.

One of the alleged victims told police that boxes in a family room had been disturbed, a bedroom closet was rummaged through, a safe in the basement was moved and copper wire had been moved from the garage to the driveway, according to court records.

Brown has denied any wrongdoing, telling police that another man working with him found that a back door had been kicked in and that it was part of his job to enter the residence to see if there were any damages or if anything was missing, records show.

Brown’s supervisor and a Bank of America representative, however, told police that no one, including Brown, was authorized to enter the residence.

The incident began at about 3:25 p.m. Oct. 18 when West Virginia State Trooper N.F. Alatta responded to a call reporting a possible burglary in progress at the home on Byron Road in southern Berkeley County.

The caller, the alleged victim’s neighbor, told Alatta that she observed two men and a woman cutting grass at the victim’s home and later saw them inside the house. The neighbor said she contacted the victim about the situation, and the victim said no one was supposed to be in the residence, records show.

The alleged victim arrived at the scene a short time later and told Alatta that she had received a letter from her bank a day earlier stating that her house had been foreclosed on. She was still moving out of the residence and had belongings inside, she told police.

At 3:42 p.m., two men arrived at the scene, one of whom was Brown. Brown told police he was contracted through Bank of America to cut the grass at the residence. He said the other man with him was helping him cut the grass when they saw the home’s back door kicked in, records show.

Read more here

Warren Edward Brown, 30, of Herman Lane, was later released after posting $15,000 bail.

One of the alleged victims told police that boxes in a family room had been disturbed, a bedroom closet was rummaged through, a safe in the basement was moved and copper wire had been moved from the garage to the driveway, according to court records.

Brown has denied any wrongdoing, telling police that another man working with him found that a back door had been kicked in and that it was part of his job to enter the residence to see if there were any damages or if anything was missing, records show.

Brown’s supervisor and a Bank of America representative, however, told police that no one, including Brown, was authorized to enter the residence.

The incident began at about 3:25 p.m. Oct. 18 when West Virginia State Trooper N.F. Alatta responded to a call reporting a possible burglary in progress at the home on Byron Road in southern Berkeley County.

The caller, the alleged victim’s neighbor, told Alatta that she observed two men and a woman cutting grass at the victim’s home and later saw them inside the house. The neighbor said she contacted the victim about the situation, and the victim said no one was supposed to be in the residence, records show.

The alleged victim arrived at the scene a short time later and told Alatta that she had received a letter from her bank a day earlier stating that her house had been foreclosed on. She was still moving out of the residence and had belongings inside, she told police.

At 3:42 p.m., two men arrived at the scene, one of whom was Brown. Brown told police he was contracted through Bank of America to cut the grass at the residence. He said the other man with him was helping him cut the grass when they saw the home’s back door kicked in, records show.

Read more here

Subscribe to:

Comments (Atom)