Citigroup Inc said it will start charging a monthly fee of $10 on checking and savings accounts with combined balances of less than $1,500, joining a growing list of banks seeking to recoup revenue lost under new financial industry regulations.

The fee will be waived if a customer completes one direct deposit and one online bill payment per month through an account, or maintains a balance of at least $1,500 in checking and savings accounts, Citigroup said on Friday

The change takes effect in December.

Under Citi's current fee structure, customers are not required to maintain minimum account balances but must complete five transactions a month through an account to avoid a monthly fee of $8.

Read on.

Saturday, September 17, 2011

Bank of America has Countrywide bankruptcy as option

Bank of America Corp. (BAC), the lender burdened by its Countrywide Financial Corp. takeover, would consider putting the unit into bankruptcy if litigation losses threaten to cripple the parent, said four people with knowledge of the firm’s strategy.

The option of seeking court protection exists because theCharlotte, North Carolina-based bank maintained a separate legal identity for the subprime lender after the 2008 acquisition, said the people, who declined to be identified because the plans are private. A filing isn’t imminent and executives recognize the danger that it could backfire by casting doubt on the financial strength of the largest U.S. bank, the people said.

The threat of a Countrywide bankruptcy is a “nuclear”option that Chief Executive Officer Brian T. Moynihan could use as leverage against plaintiffs seeking refunds on bad mortgages, said analyst Mike Mayo of Credit Agricole Securities USA. Moynihan has booked at least $30 billion of costs for faulty home loans, most sold by Countrywide during the housing boom, and analysts estimate the total could double in coming years.

Volcker rule, designed to reduce the types of risky investments blamed for triggering the financial crisis, may extend to overseas banks

Regulators writing a rule limiting proprietary trading by U.S. banks are considering extending the restrictions to overseas firms with operations in the country, according to four people familiar with the proposal.

Officials next month will issue a plan to carry out provisions of the so-called Volcker Rule, part of the Dodd-Frank financial-regulation law. The purpose is to clarify what types of offshore trading are exempt from the Volcker Rule, the people said.

The Volcker Rule, designed to reduce the types of risky investments blamed for triggering the financial crisis, has prompted U.S. banks such as Goldman Sachs Group Inc. (GS) to close proprietary-trading operations. Overseas banks say that a strict interpretation of the rule may also force them to fire or relocate U.S. employees who are involved in proprietary trading, even if no American money is at risk.

Scott Walker, Wisconsin Governor, Eyed In Corruption Probe After FBI Raid On Cynthia Archer's Home

MILWAUKEE — Wisconsin Gov. Scott Walker said Friday all he knows about FBI agents seizing items from the home of one of his top agency officials is what he's seen in the media and that his office has not been told anything about the raid.

The first-term governor said "it's hard to tell" whether he should be concerned about Wednesday's raid on the home of Cynthia Archer, who was his aide while Milwaukee County executive and followed him to work in state government when he was elected governor.

"We don't know what exactly is involved," Walker said Friday when asked about the raid following an unrelated event in Milwaukee.

"Until we know, obviously it's a concern but again, I don't know any more details than what I've seen reported in the media outlets around the state," he added.

The raid came amid a secret Milwaukee County investigation that the Milwaukee Journal Sentinel, citing unnamed people familiar with the case, has reported focuses on whether county staffers in Walker's office did political work on the taxpayer dime.

Read on.

The first-term governor said "it's hard to tell" whether he should be concerned about Wednesday's raid on the home of Cynthia Archer, who was his aide while Milwaukee County executive and followed him to work in state government when he was elected governor.

"We don't know what exactly is involved," Walker said Friday when asked about the raid following an unrelated event in Milwaukee.

"Until we know, obviously it's a concern but again, I don't know any more details than what I've seen reported in the media outlets around the state," he added.

The raid came amid a secret Milwaukee County investigation that the Milwaukee Journal Sentinel, citing unnamed people familiar with the case, has reported focuses on whether county staffers in Walker's office did political work on the taxpayer dime.

Read on.

BofA, JPMorgan Fail to Make Fannie Mae Grade for Loan Servicing

Bank of America Corp. (BAC), the largest U.S. mortgage servicer, failed to make a list of companies doing a satisfactory job of assisting homeowners struggling to pay their mortgage, according to Fannie Mae.

Of the 11 biggest servicers of Fannie Mae mortgages, Wells Fargo & Co. (WFC), Citigroup Inc. (C), Ally Financial Inc. and EverBank Financial Corp. are on track to receive satisfactory or better grades under a newly created customer service and foreclosure- prevention ratings system, the mortgage-finance company said in a statement. JPMorgan Chase & Co. (JPM), SunTrust Banks Inc. (STI), PHH Corp. (PHH), PNC Financial Services Group Inc. (PNC), OneWest Bank FSB and MetLife Inc. (MET) were the other companies that didn’t make the list.

“Servicers who achieve the highest ratings are leading the way in providing assistance to homeowners who are having difficulty making their mortgage payments,” Leslie Peeler, vice president of servicer portfolio management for Washington-based Fannie Mae, said in the statement yesterday.

Check out the rest here…

Of the 11 biggest servicers of Fannie Mae mortgages, Wells Fargo & Co. (WFC), Citigroup Inc. (C), Ally Financial Inc. and EverBank Financial Corp. are on track to receive satisfactory or better grades under a newly created customer service and foreclosure- prevention ratings system, the mortgage-finance company said in a statement. JPMorgan Chase & Co. (JPM), SunTrust Banks Inc. (STI), PHH Corp. (PHH), PNC Financial Services Group Inc. (PNC), OneWest Bank FSB and MetLife Inc. (MET) were the other companies that didn’t make the list.

“Servicers who achieve the highest ratings are leading the way in providing assistance to homeowners who are having difficulty making their mortgage payments,” Leslie Peeler, vice president of servicer portfolio management for Washington-based Fannie Mae, said in the statement yesterday.

Check out the rest here…

Friday, September 16, 2011

Issa launches probe of Fannie, BofA mortgage servicing deal

Rep. Darrell Issa (R-Calif.), chairman of the House Oversight and Government Reform Committee, opened an investigation into the reported Fannie Mae purchase of a Bank of America (BAC: 7.33 +3.97%) mortgage servicing portfolio.

According to the Wall Street Journal, the deal was finalized in August. The portfolio includes 400,000 loans with an unpaid principal balance of $73 billon and a delinquency rate of 13%, twice the national average. Fannie reportedly paid $500 million for it.

"Some commentators have labeled this transaction as a back-door bailout of BofA by permitting the bank to shift part of its risky portfolio to American taxpayers. Under these circumstances, I am unclear why the Federal Housing Finance Agency allowed Fannie to proceed with the transaction," Issa wrote in a letter to FHFA Acting Director Edward DeMarco.

Thursday, September 15, 2011

Bank of America to pay whistle-blower $930,000

The Labor Department ordered Bank of America (BAC: 7.05 +0.71%) to reinstate and pay $930,000 to an employee, who was fired after reporting instances of possible fraud among Countrywide Financial Corp. employees.

The Labor Department's Occupational Safety and Health Administration division in San Francisco launched an investigation after a Los Angeles-based employee filed a complaint, claiming the lender violated a federal whistle-blower protection law.

Wednesday, September 14, 2011

Biloxi Buzz for Wednesday

U.S. Poverty Rate Hits Highest Level Since 1993

Perry Faces Backlash Over In-State Tuition For Undocumented Students

Clergy Sex Abuse Victims File International Court Case Against Pope

Last week's poll had asked:

What do you fear most? JL readers answered none of the above. This week's poll is now up.

NY Judge Throw Down Gauntlet On Bank Servicers For Acting In Bad Faith

Dental hygienist Charmaine Davis’ ordeal with Deutsche Bank began soon after she found herself facing foreclosure while helping her mother deal with cancer.

After 17 negotiation conferences, her effort to modify her loan had gone nowhere – until a Brooklyn judge stepped in and punished the bank for “bad faith” bargaining.

Davis’ case is hardly unique. Banks have come under increasing fire for mishandling the growing number of foreclosed properties on their books.

More and more distressed homeowners have complained that lenders refuse to work with them to modify loans so they can keep their properties and continue paying down their debt.

In 2009 a New York law began requiring banks to make a “good faith effort” to negotiate with homeowners and try to work something out. In recent months judges have begun cracking down on banks that don’t make that “good faith” effort.

From November 2009 through last month, New York judges have slammed banks for their lack of good faith in at least seven cases. In one case a judge ordered the mortgage debt wiped out. In the others substantial sanctions were imposed or threatened.

In Davis’ case, she had promised her mother she would do everything she could to keep her Midwood, Brooklyn, house, and at first, she figured she could work something out. “I didn’t want her dying thinking it was because she got sick that I was in this situation,” she said.

Starting in April 2009, she began attending settlement conferences with the bank to try and modify the loan. Her mother died in December 2009, and through February of this year Davis participated in 17 conferences – about one every five weeks.

During that time, the bank lost her first three applications for a loan modification. She submitted five in total. “Everything they required – even it if was the tip of the needle – we gave them,” she said.

In February 2010, the bank said it could neither offer nor deny a modification because Davis had failed to provide a tax return for self-employed persons.

Davis had never been self-employed.

Read more here

After 17 negotiation conferences, her effort to modify her loan had gone nowhere – until a Brooklyn judge stepped in and punished the bank for “bad faith” bargaining.

Davis’ case is hardly unique. Banks have come under increasing fire for mishandling the growing number of foreclosed properties on their books.

More and more distressed homeowners have complained that lenders refuse to work with them to modify loans so they can keep their properties and continue paying down their debt.

In 2009 a New York law began requiring banks to make a “good faith effort” to negotiate with homeowners and try to work something out. In recent months judges have begun cracking down on banks that don’t make that “good faith” effort.

From November 2009 through last month, New York judges have slammed banks for their lack of good faith in at least seven cases. In one case a judge ordered the mortgage debt wiped out. In the others substantial sanctions were imposed or threatened.

In Davis’ case, she had promised her mother she would do everything she could to keep her Midwood, Brooklyn, house, and at first, she figured she could work something out. “I didn’t want her dying thinking it was because she got sick that I was in this situation,” she said.

Starting in April 2009, she began attending settlement conferences with the bank to try and modify the loan. Her mother died in December 2009, and through February of this year Davis participated in 17 conferences – about one every five weeks.

During that time, the bank lost her first three applications for a loan modification. She submitted five in total. “Everything they required – even it if was the tip of the needle – we gave them,” she said.

In February 2010, the bank said it could neither offer nor deny a modification because Davis had failed to provide a tax return for self-employed persons.

Davis had never been self-employed.

Read more here

Michigan Counties Can Ban Owners From Foreclosure Resales

State officials and area county treasurers say Wayne County already has the authority to stop a growing number of property owners from ditching tax debt by buying their land back for pennies on the dollar at the annual foreclosure auction.

But Wayne County officials said they don’t want to ban the practice, arguing it would be too hard to enforce and could hurt poor homeowners.

“We have no plan to do that at this point,” said Wayne County Chief Deputy Treasurer David Szymanski. “The enforcement mechanism for not allowing people to buy back is a nightmare.”

“We are trying the do the best we can in trying economic times.”

The Detroit News reported last week that Detroit property owners are using the little-known loophole to erase tax debt, interest, fees and unpaid water bills by letting properties go into foreclosure and then buying them back at the Wayne County treasurer’s auction, sometimes for as low as $500.

The News identified about 200 of nearly 3,700 Detroit properties sold at auction last year that appeared to be bought back by owners, wiping away about $1.8 million in tax debt.

That included one Detroit landlord who lost seven rentals after he didn’t pay $131,800. He bought them back a month later for $4,051.

At the September auction, the properties’ prices are the debt that’s owed. But in October, the county treasurer sells off whatever is left at a $500 opening bid.

While Wayne County doesn’t want to stop the method, Macomb County Treasurer Ted Wahby said he plans to officially ban the practice this fall. His office is drafting a registration form that would make the buyer pledge that they are not buying back their property and if found lying, the sale would be voided.

“As the economic situation is getting worse, it opens the doors to these guys,” Wahby said. “If they are allowed to get away with that, you’ll see this hole it will create for the county.”

Wahby said he hasn’t seen anyone try it yet, but he is worried about the potential and wasn’t sure he could prevent it. This spring he asked state Sens. Steven Bieda and Jack Brandenburg to push legislation to ban it. But after the bill’s introduction, state Treasurer Andy Dillon’s office said county treasurers already had that power.

But Wayne County officials said they don’t want to ban the practice, arguing it would be too hard to enforce and could hurt poor homeowners.

“We have no plan to do that at this point,” said Wayne County Chief Deputy Treasurer David Szymanski. “The enforcement mechanism for not allowing people to buy back is a nightmare.”

“We are trying the do the best we can in trying economic times.”

The Detroit News reported last week that Detroit property owners are using the little-known loophole to erase tax debt, interest, fees and unpaid water bills by letting properties go into foreclosure and then buying them back at the Wayne County treasurer’s auction, sometimes for as low as $500.

The News identified about 200 of nearly 3,700 Detroit properties sold at auction last year that appeared to be bought back by owners, wiping away about $1.8 million in tax debt.

That included one Detroit landlord who lost seven rentals after he didn’t pay $131,800. He bought them back a month later for $4,051.

At the September auction, the properties’ prices are the debt that’s owed. But in October, the county treasurer sells off whatever is left at a $500 opening bid.

While Wayne County doesn’t want to stop the method, Macomb County Treasurer Ted Wahby said he plans to officially ban the practice this fall. His office is drafting a registration form that would make the buyer pledge that they are not buying back their property and if found lying, the sale would be voided.

“As the economic situation is getting worse, it opens the doors to these guys,” Wahby said. “If they are allowed to get away with that, you’ll see this hole it will create for the county.”

Wahby said he hasn’t seen anyone try it yet, but he is worried about the potential and wasn’t sure he could prevent it. This spring he asked state Sens. Steven Bieda and Jack Brandenburg to push legislation to ban it. But after the bill’s introduction, state Treasurer Andy Dillon’s office said county treasurers already had that power.

Huge Surge in Bank of America Foreclosures

Bank of America is ramping up its foreclosure processing, sending out far more notices of default to borrowers in August than in previous months, well over 200 percent more month-to-month.

A notice of default is the first stage of the foreclosure process in non-judicial foreclosures states, that is, where foreclosures do not go before a judge.

The notice of default is usually sent when a borrower is 90 days or more overdue in payments, but that timeline has been extended significantly during this housing crisis, due to the so-called "robo-signing" processing scandal and the sheer volume of troubled loans.

Read on.

A notice of default is the first stage of the foreclosure process in non-judicial foreclosures states, that is, where foreclosures do not go before a judge.

The notice of default is usually sent when a borrower is 90 days or more overdue in payments, but that timeline has been extended significantly during this housing crisis, due to the so-called "robo-signing" processing scandal and the sheer volume of troubled loans.

Read on.

Tuesday, September 13, 2011

Deutsche Bank VP sues, alleges bias over pregnancy

NEW YORK, Sept 12 (Reuters) - A Deutsche Bank AG (DBKGn.DE) vice president filed a gender bias lawsuit accusing the German bank of denying her pay and promotions, and trying to demote her because she took maternity leave.

Kelley Voelker, who works in New York in a hedge fund group, said she has never been promoted in her 13 years at Deutsche Bank despite being qualified to become a director.

Voelker, who is in her mid-40s, sued the bank in papers filed Monday in U.S. District Court in Manhattan.

"We take these allegations very seriously and are currently reviewing the complaint," a Deutsche Bank spokeswoman said

Kelley Voelker, who works in New York in a hedge fund group, said she has never been promoted in her 13 years at Deutsche Bank despite being qualified to become a director.

Voelker, who is in her mid-40s, sued the bank in papers filed Monday in U.S. District Court in Manhattan.

"We take these allegations very seriously and are currently reviewing the complaint," a Deutsche Bank spokeswoman said

CFPB launches fourth round of mortgage disclosure form testing

The Consumer Financial Protection Bureau launched a fourth round of testing Monday as the agency collects feedback about sample mortgage disclosure forms that will help the agency construct standard uniform lending documents for the industry.

The CFPB's "Know Before You Owe" campaign posted identical mortgage forms online this week with different loan products printed on each form for the purpose of testing how well the disclosure documents communicate differences between loan products printed on the same form.

During the first three rounds of testing, the CFPB collected feedback on various disclosure forms to compare the pros and cons of each. In the new test, the CFPB will compare two identical forms with different loan information to see how clear the price differences are to consumers and lenders who read the documents.

Citigroup, JPMorgan Chase Only U.S. Banks Significantly Exposed To European Crisis: Analyst

Rochdale Securities' analyst Richard Bove said fears of a possible impact of a European debt crisis on U.S. banks were overblown, with only Citigroup and JP Morgan Chase having a significant exposure to the crisis.

"Assuming some relatively worse case developments, it appears that Citigroup and JP Morgan Chase are at risk to the developments in Europe. No other American institution is," Bove wrote in a note.

Citing the filings from the International Financial Statistics Yearbook, released by the International Monetary Fund for the year 2010, Bove said Citigroup is at biggest risk with exposure of $12.3 billion in Italy and $10.8 billion in Spain.

JP Morgan Chase risks write downs on the $18.8 billion it loaned to Ireland, $12.2 billion to Italy and $12 billion to Spain, according to the filings.

The brokerage ruled out any risks from limited exposure to either Goldman Sachs, or Morgan Stanley and termed the exposure amount "not significant."

"Assuming some relatively worse case developments, it appears that Citigroup and JP Morgan Chase are at risk to the developments in Europe. No other American institution is," Bove wrote in a note.

Citing the filings from the International Financial Statistics Yearbook, released by the International Monetary Fund for the year 2010, Bove said Citigroup is at biggest risk with exposure of $12.3 billion in Italy and $10.8 billion in Spain.

JP Morgan Chase risks write downs on the $18.8 billion it loaned to Ireland, $12.2 billion to Italy and $12 billion to Spain, according to the filings.

The brokerage ruled out any risks from limited exposure to either Goldman Sachs, or Morgan Stanley and termed the exposure amount "not significant."

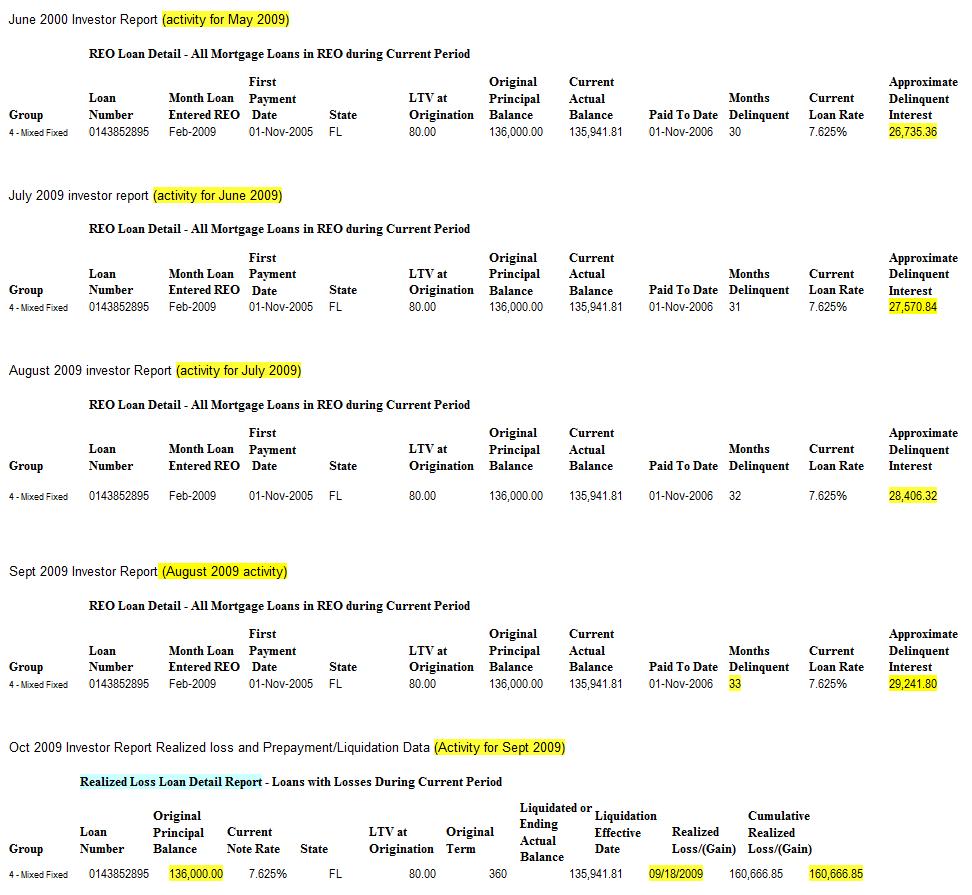

Another loan in the FHFA v BoA lawsuit – interest accrual for months after home is “liquidated” to new party

Another loan in a trust/tranche that is named in the FHFA v BoA lawsuit. This loan is in collateral group 4 in STALT 2005-1F trust.

This loan, for $136,000, was stated to be an 80% LTV but there was a 20% loan ($25,500) originated on the same day, buy the same originator, Suntrust/MERS.

Property sold to third party buyer on June 2, 2009 for $49,338 (see property appraiser site here) but not reported as “liquidated” until Sept 2009. The delinquent interest accrued in June, July, and August 2009 = $2506.

This loan’s cumulative loss booked to the trust is $160,666.85. (remember that the original loan balance was $136,000)

How are the proceeds from the sale, $49,338, accounted for? What is the meaning of the delay in reporting the “liquation date” and the additional months of interest accural?

Here is the warranty deed in Palm Beach County Official Records 23443/0469

Monday, September 12, 2011

Bank of America in the spotlight Monday; Open thread

SEC Bans Document Destruction After Whistleblower Cries Foul

The Securities and Exchange Commission has forbidden its employees from destroying investigative documents, as fallout spreads from a whistleblower’s recent claim that the agency has illegally destroyed thousands of preliminary investigation documents.

An SEC attorney alerted Sen. Chuck Grassley (R-Iowa) of the possible crimes in August. The whistleblower said the documents in question were “matters under inquiry,” including reviews of AIG, Morgan Stanley, Lehman Brothers and Bernie Madoff.

“This agency has been in knots over its documents policy,” said Grassley, who has requested more information from SEC Chairman Mary Shapiro. ”It makes sense to stop destroying records until it figures this out. The agency and the National Archives need to determine what records have to be kept, both for what’s logical for investigations and what’s necessary under federal law.”

The SEC’s internal watchdog is investigating the agency’s document policies and will release reports this month.

“We have been working with [the National Archives and Records Administration] on a new policy for records retention, and have determined to suspend the current policy out of an abundance of caution until a new policy is in place,” said an SEC spokesman.

An SEC attorney alerted Sen. Chuck Grassley (R-Iowa) of the possible crimes in August. The whistleblower said the documents in question were “matters under inquiry,” including reviews of AIG, Morgan Stanley, Lehman Brothers and Bernie Madoff.

“This agency has been in knots over its documents policy,” said Grassley, who has requested more information from SEC Chairman Mary Shapiro. ”It makes sense to stop destroying records until it figures this out. The agency and the National Archives need to determine what records have to be kept, both for what’s logical for investigations and what’s necessary under federal law.”

The SEC’s internal watchdog is investigating the agency’s document policies and will release reports this month.

“We have been working with [the National Archives and Records Administration] on a new policy for records retention, and have determined to suspend the current policy out of an abundance of caution until a new policy is in place,” said an SEC spokesman.

New rule to require banks to make a 'living will'

U.S. banks preparing to submit plans on how they can be put to death are pushing regulators to put more emphasis on how to keep them alive.

This week, U.S. regulators are set to unveil a final rule that requires banks and some other large financial companies to write "living wills" that provide a road map for how they could be quickly liquidated if they run into trouble.

The rule is required by the 2010 Dodd-Frank financial oversight law, and the Federal Deposit Insurance Corp (FDIC) board is scheduled to vote on Tuesday on the final rule. The Federal Reserve also would have to approve the rule before it takes effect, most likely in about a month.

Banking executives and consultants working for large banks say the rule should include room for what a financial institution would do to nurse itself back to health and avoid having to be liquidated.

Jamie Dimon, CEO Of JPMorgan Chase, Calls International Bank Rules 'Anti-American'

The United States should consider pulling out of the Basel group of global regulators, Jamie Dimon, chief executive of JPMorgan Chase, said in an interview with the Financial Times.

Dimon said he was supportive of forcing banks to have more capital but argued that moves to impose an additional charge on the largest global banks went too far, particularly for U.S. lenders.

He was quoted as describing new international bank capital rules as "anti-American".

"I'm very close to thinking the U.S. shouldn't be in Basel anymore. I would not have agreed to rules that are blatantly anti-American," he said in the interview.

"Our regulators should go there and say: 'If it's not in the interests of the U.S., we're not doing it'."

The Basel III capital rules are designed to increase the safety of the financial system by making banks build up risk-absorbent "core tier one" capital to at least 7 percent of risk-weighted assets. The biggest, including JPMorgan, have to reach 9.5 percent.

Sunday, September 11, 2011

Disabled homeowner alleges Emigrant Mortgage sold her a mortgage she couldn’t afford

Margaret Mosunic is 63 and a devout Christian, but if she ever encounters her building contractor again, she has a specific, violent plan of action.

“I want to choke his little Irish neck,” she said in a recent interview in her home of more than 40 years in Queens, New York.

As for the mortgage broker who recommended the contractor? “[He is] a devil in the disguise of a man,” she said.

On Jan. 9, 2008, Thomas Delaney, a broker at Home Consultants, Inc., drove Mosunic to a law office to close what she thought was a $40,000 bank loan, according to a lawsuit filed by Mosunic in Queens County court. She planned to use the money to pay back taxes and make repairs to a downstairs rental apartment, she said.

But that wasn’t the loan that the broker had asked the lender, Emigrant Mortgage Co. of New York to approve, Mosunic’s lawsuit alleges.

An hour later, Mosunic claims, she stood on a street corner with a $20 bill that Delaney had pressed into her hand for cab fare, confused and upset. She had just signed her name to a $300,000 mortgage with terms she alleges she couldn’t possibly meet.

Mosunic’s loan required a monthly payment of $2,227. At the time, her only income was a $738 monthly disability check.

“I was flabbergasted and I was so upset,” Mosunic said when she got her first bill.

The interest rate on the loan was 8.125 percent. But if she missed a single payment by more than 30 days, the rate would jump up to a “default” rate of 18 percent. If that happened, her monthly bill would double, to about $4,500 a month.

While Mosunic was obligated to make payments on the full loan amount, the bank held back half—$150,000—in escrow, with its release contingent on repairs to a downstairs apartment.

Emigrant Bank, the parent of Emigrant Mortgage, said in written answers to questions from iWatch News that loan documents prove Mosunic knew in advance of the closing the amount of her mortgage loan.

The bank said withholding two times the amount estimated to complete repairs is “usual practice” and that Mosunic could have afforded the payments if the renovation had been completed. Then Mosunic would have received the rest of her loan and she could have brought in a tenant, the bank said.

But that didn’t happen. The contractor she hired, at the broker Delaney’s suggestion, took $70,000 and left the job half-done, she alleges in her lawsuit. She says back taxes and bills ate up most of the rest of the $150,000.

She made two mortgage payments. The foreclosure notice came in September 2008.

In the run-up to the housing collapse, millions of borrowers with bad credit bought homes that they couldn’t afford and have since lost to foreclosure.

Mosunic, who moved to New York City from Croatia when she was a teenager, does not fit the usual profile of those borrowers. She owned her house in the Astoria neighborhood outright. She has lived there since the 1960s.

But a low income and poor credit history made borrowing money difficult. With a huge tax bill, payment due on heating oil, and other debt, she needed money badly.

Enter Emigrant Bank, which offered a program that allowed homeowners to borrow about half of their home’s appraised value without having to provide proof of income. The home was the collateral.

In a court filing contesting the foreclosure, Mosunic claims the lender, broker and contractor took advantage of her disability—she says she is legally blind and reads very slowly—and her limited education.

U.S. Obtains Data From 10 Swiss Banks In Tax-Dodging Probe

ZURICH - U.S. authorities now have statistical data from the ten Swiss banks being investigated by the United States for helping U.S. clients to dodge taxes, Swiss newspaper Neue Zuercher Zeitung reported on Saturday.

TagesAnzeiger, another Swiss newspaper, reported that the Swiss banks now had until Sept 23 to hand over more specific client data.

Credit Suisse , which is one of the banks under investigation, had already handed over data earlier in the week, while the nine other banks had handed over the data through an intermediary on Friday, NZZ said without citing any sources.

The newspaper also said the Swiss government had given them "plenty of rope" to do this.

Mario Tuor, spokesman for the Swiss department for international financial affairs, declined to comment on the NZZ and TagesAnzeiger reports, but he said: "We are still going for a solution on the basis of existing legal rules in Switzerland."

Late on Friday, Reuters reported that the United States was drafting legal documents, seeking to force nearly a dozen Swiss banks and international banks with Swiss branches to disclose the identities of American clients that evaded taxes.

TagesAnzeiger, another Swiss newspaper, reported that the Swiss banks now had until Sept 23 to hand over more specific client data.

Credit Suisse , which is one of the banks under investigation, had already handed over data earlier in the week, while the nine other banks had handed over the data through an intermediary on Friday, NZZ said without citing any sources.

The newspaper also said the Swiss government had given them "plenty of rope" to do this.

Mario Tuor, spokesman for the Swiss department for international financial affairs, declined to comment on the NZZ and TagesAnzeiger reports, but he said: "We are still going for a solution on the basis of existing legal rules in Switzerland."

Late on Friday, Reuters reported that the United States was drafting legal documents, seeking to force nearly a dozen Swiss banks and international banks with Swiss branches to disclose the identities of American clients that evaded taxes.

Subscribe to:

Comments (Atom)