THE mortgage business is moribund. New loans are down. New foreclosures are up. But why let a little sorry news get in the way of a good party? Last week, almost 3,000 people descended on the Hyatt Regency in Chicago for the 98th annual convention of the Mortgage Bankers Association.

The price of admission: about $1,000 a head. But for that grand, you got to hear the band Chicago play hits from the ’70s. And David Axelrod and Jeb Bush give speeches. And experts discuss things like demographics, the politics of housing and the future of the mortgage industry, according to a flier for the event.

“Gather the information you need to help your business and our industry drive change,” the pitch went.

The city of Chicago was no doubt grateful for the conventioneers’ dollars. Besides, Mayor Rahm Emanuel knows something about this industry: he used to be a director at the mortgage giant Freddie Mac.

Nothing wrong with a bit of schmoozing. But it might seem jarring that Freddie, which was rescued by Washington and today exists at the pleasure of taxpayers, paid $80,000 to become a “platinum” sponsor of this shindig. Fannie Mae, that other ward of the state, paid $60,000 to become a “gold” sponsor.

Keep in mind that taxpayers bailed out Fannie and Freddie to the tune of about $150 billion.

Today, Fannie and Freddie are about the only games in mortgage town. Yes, banks make loans, but more often than not they hand them off to one of the two. So it’s a mystery why Fannie and Freddie needed to help foot the bill for the gathering.

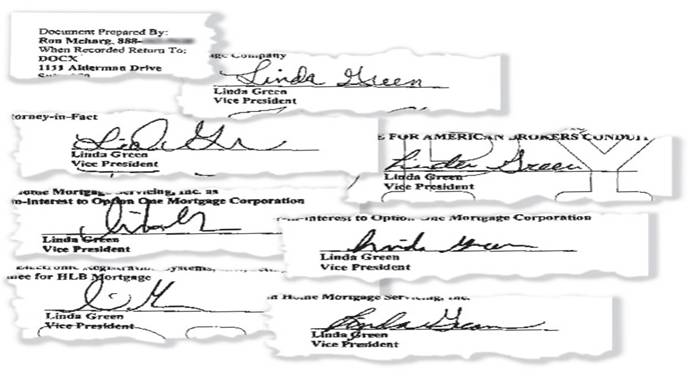

Freddie’s companions in the platinum sponsor list make for interesting reading. One was the Mortgage Electronic Registration System, or MERS, which has repeatedly foreclosed on troubled homeowners and made a hash of the nation’s real estate records. Another was Lender Processing Services of Florida, which made robo-signing a household word.

MERS and Lender Processing Services are at the center of the foreclosure crisis. Why would Freddie keep such company?

Perhaps more disturbing is that Fannie and Freddie sent an army of their own to Chicago: 87 people in all. According to a list of registrants, that’s more than hailed from the Mortgage Bankers Association (60 people), Bank of America (58), Wells Fargo (54) and JPMorgan Chase (24).